“Discover the 4 top investment choices—Index Funds, Mutual Funds, ETFs, and Fixed Deposits. Learn the best option for your financial goals, risk appetite, and investment horizon. Empower your investment strategy with this comprehensive guide!”

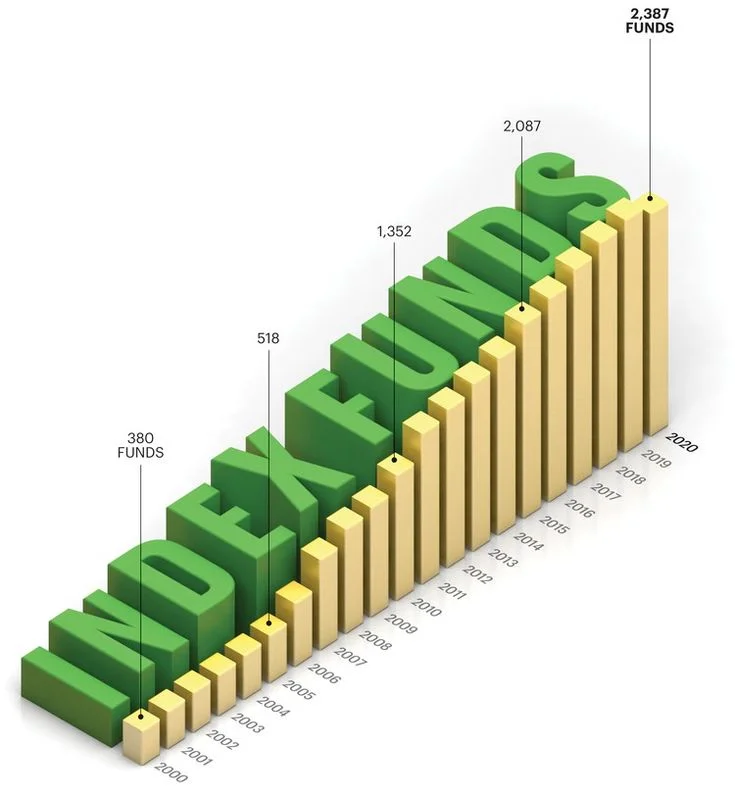

1. Index Funds: A Simple Way to Invest in the Market

One of the biggest advantages of index funds is their low cost. Since there’s no active management involved, the expense ratio (fees charged to manage the fund) is much lower compared to mutual funds. This makes them an attractive choice for long-term investors who want to minimize costs and benefit from market growth.

Think of index funds as an “autopilot” way to invest in the stock market. They’re like a basket that holds shares of companies listed in a market index, such as the Nifty 50 or Sensex.

- Low Fees: Since they don’t need fancy fund managers, the costs are lower.

- Easy Diversification: Your money spreads across many companies, reducing risk.

- No Complications: They simply follow the market, with no surprises.

Best For: If you want a low-maintenance, cost-effective way to grow your wealth over the years, index funds are a solid choice.

2. Mutual Funds: Let the Experts Do the Work

Mutual funds are investment vehicles that pool money from multiple investors which has multiple option invest in stocks, bonds, or other assets. Managed by professional fund managers, they offer diversification and cater to various risk levels, from aggressive equity funds to stable debt funds.

Mutual funds are like hiring a professional chef to cook your financial meal. A fund manager actively chooses where to invest, aiming to beat the market.

- Professional Management: Someone experienced is making decisions for you.

- Lots of Options: There’s a mutual fund for every risk level and goal.

- Diversification: You’re investing in a mix of assets, which spreads out risk.

Best For: If you like the idea of having an expert guide your investments and don’t mind paying higher fees for the potential of better returns, mutual funds could work for you.

3. ETFs: The Best of Both Worlds

One of the main advantages of ETFs is their real-time trading. Unlike mutual funds, which can only be bought or sold at the end of the trading day, ETFs can be traded throughout the day at market prices. This makes them a flexible option for investors who prefer more control over their investments.

ETFs (Exchange-Traded Funds) are like a mix between index funds and stocks. They track an index (like index funds) but trade on the stock market, so you can buy or sell them throughout the day.

- Low Costs: They’re inexpensive, just like index funds.

- Trading Flexibility: You can buy or sell whenever the market is open.

- Tax Efficiency: They’re usually more tax-friendly than mutual funds.

Best For: If you want a cost-effective investment with the ability to trade like a stock and have a Demat account, ETFs are a great pick.

4. Fixed Deposits: The Safe and Steady Option

Fixed Deposits (FDs) are the no-drama choice. You give your money to the bank, and they pay you a fixed interest rate. No surprises.

- Zero Risk: Your money is safe, and you know exactly how much you’ll get back.

- Good for Short-Term Goals: If you need the money soon, it’s a secure place to park it.

- Tax Savings: Some FDs give tax benefits under Section 80C.

Best For: If you’re risk-averse or need a reliable option for short-term goals, FDs are your friend.

So, Which One is Right for You?

It all depends on what you want:

- Willing to Take Some Risk for Higher Returns? Index funds, mutual funds, or ETFs are worth considering, especially if you’re thinking long-term.

- Prefer Safety and Guaranteed Returns? Fixed Deposits are your best bet, particularly for short-term financial goals.

- Want Low-Cost, Hands-Off Investing? Index funds and ETFs are ideal if you don’t want to micromanage your investments.

- Okay Paying More for Active Management? Mutual funds are a good option if you’re willing to spend extra for professional help.

Quick Comparison

Index funds, mutual funds, ETFs, and fixed deposits are popular investment options, each catering to different financial needs. Index funds are passively managed funds that track specific market indices, such as the Nifty 50, offering low-cost diversification and moderate risk. They are best suited for long-term investors seeking steady growth with minimal management. Mutual funds, on the other hand, are actively managed by professional fund managers and offer a wide range of options, including equity, debt, and hybrid funds. They cater to investors with varying risk appetites and goals but come with slightly higher fees and varying levels of risk depending on the type of fund.

ETFs (Exchange-Traded Funds) provide the diversification benefits of index funds but trade like stocks on exchanges, offering real-time liquidity and flexibility. They are ideal for DIY investors looking for low-cost options and the ability to trade during market hours. Finally, fixed deposits (FDs) are a safe and predictable choice for risk-averse investors. FDs guarantee returns and are perfect for short-term goals or preserving capital, though they may not outpace inflation in the long run. Each option has its strengths, so selecting the right one depends on your financial goals, risk tolerance, and investment timeline.

- Index Funds: Great for beginners who want simplicity and low fees.

- Mutual Funds: Good for people who like the idea of active management.

- ETFs: Perfect for investors who want flexibility and lower costs but don’t mind using a trading account.

- Fixed Deposits: Ideal for risk-averse people who need steady, guaranteed returns.

Conclusion

In conclusion, choosing the right investment option—whether it’s index funds, mutual funds, ETFs, or fixed deposits—depends on your financial goals, risk appetite, and investment timeline. Each option offers unique benefits and challenges, making it essential to understand their features before making a decision.

Index funds are ideal for those who seek simplicity and steady long-term growth. They replicate market indices like the Nifty 50 or S&P 500, offering broad diversification at a low cost. For investors with a long-term horizon and moderate risk tolerance, index funds are a reliable way to build wealth without the need for constant monitoring. However, they lack the flexibility of active management and may not outperform the market.

Mutual funds, on the other hand, cater to a wide variety of investors with different goals. From equity funds for aggressive growth to debt funds for stability, mutual funds provide actively managed options tailored to specific needs. While they offer the potential for higher returns, they also come with higher expense ratios and the risk of underperformance compared to benchmarks. Investors who value professional management and have varying risk appetites may find mutual funds appealing.

ETFs (Exchange-Traded Funds) combine the benefits of index funds and stocks. They provide diversification like index funds but trade on the stock exchange, offering liquidity and real-time pricing. ETFs are an excellent choice for those who prefer low costs, transparency, and the ability to trade throughout the day. However, they require a brokerage account and may involve transaction fees. For investors who value flexibility and are comfortable managing their investments, ETFs can be a great option.

Fixed deposits (FDs) are the go-to choice for risk-averse investors seeking capital preservation and guaranteed returns. FDs offer stability and predictable income, making them a preferred option for short-term goals or creating an emergency fund. However, their returns are often lower than inflation in the long run, limiting their growth potential. For conservative investors or retirees looking for safe and stable returns, fixed deposits remain a reliable choice.

Ultimately, no single investment option fits all needs. A well-balanced investment strategy often involves a mix of these options, tailored to your financial goals. For example, younger investors with a longer time horizon may prioritize index funds, mutual funds, or ETFs for growth, while those nearing retirement may lean toward fixed deposits for stability. Diversification across asset classes ensures that you minimize risk while optimizing returns.

It’s also essential to review your investments regularly, especially as your life goals, financial needs, and market conditions change. Rebalancing your portfolio ensures that it continues to align with your objectives.

In a world where financial literacy is increasingly important, understanding these four investment options equips you to make informed decisions that can secure your financial future. Whether you’re aiming for long-term wealth creation, consistent income, or capital preservation, there’s an investment choice for everyone. Take the time to research, seek professional advice if needed, and start investing today—your future self will thank you for it.

Feel free to reach out or leave a comment if you have questions or want personalized investment advice. Happy investing!

For more information, visit:- Investment Plans: 30 Best Investment Plans for High Long Term Returns in 2024 | Max Life Insurance

Pingback: 15 Must-Have Documents for a Perfect International Travel