On This Page

SBI vs HDFC Savings Account 2026 - Both at 2.50% Interest

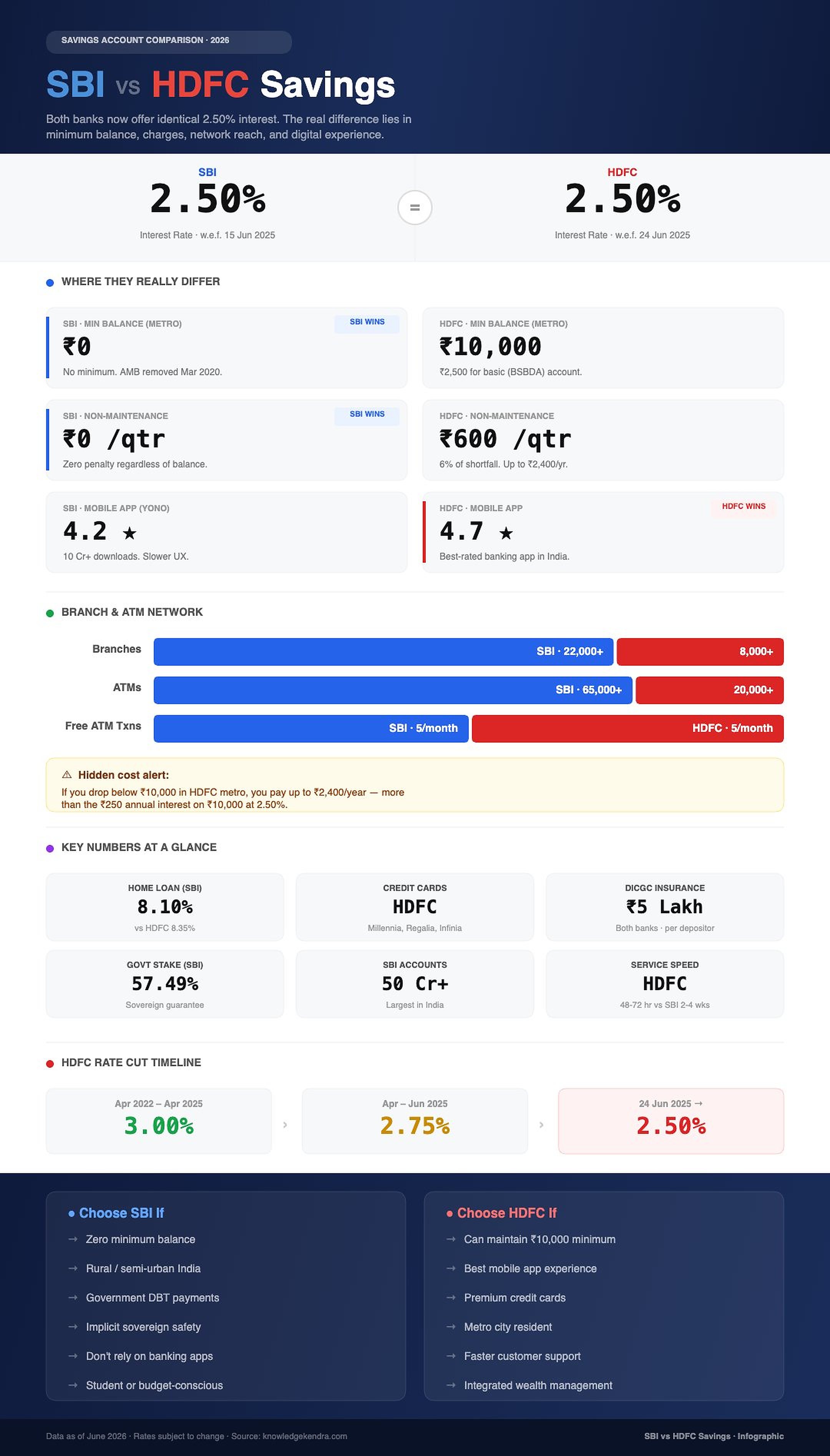

Both SBI and HDFC now offer 2.50% on savings (mid-2025 rate cut). Real difference: SBI has ₹0 minimum balance vs HDFC ₹10,000 + ₹150-600 quarterly charges. SBI wins on cost, HDFC on digital app.

📊SBI vs HDFC: Complete Feature Comparison

| Feature | SBI | HDFC Bank |

|---|---|---|

| Interest Rate (< ₹50 crore) | 2.70-3.00% | 3.00-3.25% |

| Minimum Balance (Metro) | ₹3,000 (Regular); ₹0 (BSBD) | ₹10,000 (Regular); ₹2,500 (Basic) |

| Non-maintenance charge | ₹5-15/month + 18% GST | ₹150-600/quarter + 18% GST |

| ATM network | 70,000+ ATMs (largest in India) | 20,000+ ATMs (3rd largest) |

| Branch network | 22,000+ branches (largest, deep rural reach) | 8,000+ branches (metro/tier-1 focused) |

| Mobile banking app | YONO (improving, user-friendly) | HDFC Mobile Banking (excellent, fastest) |

| UPI/Digital payments | Yes (BHIM, YONO) | Yes (PhonePe, PayZapp integration) |

| Customer service speed | Average (2-4 weeks for requests) | Good (48-72 hour response, dedicated RM) |

| Government scheme integration | Best (DBT, Jan Dhan, PM Kisan auto-linked) | Good (all schemes available) |

| Debit card options | RuPay, Visa (basic to premium) | Visa, Mastercard (premium options) |

| FD rates (1-year) | 6.50-7.10% | 7.00-7.25% |

| Home loan rates | Slightly lower (PSU advantage, 8.3-8.5%) | Competitive (8.5-8.75%) |

| Credit cards | SimplyCLICK, Elite (decent) | Millennia, Regalia, Infinia (industry-best) |

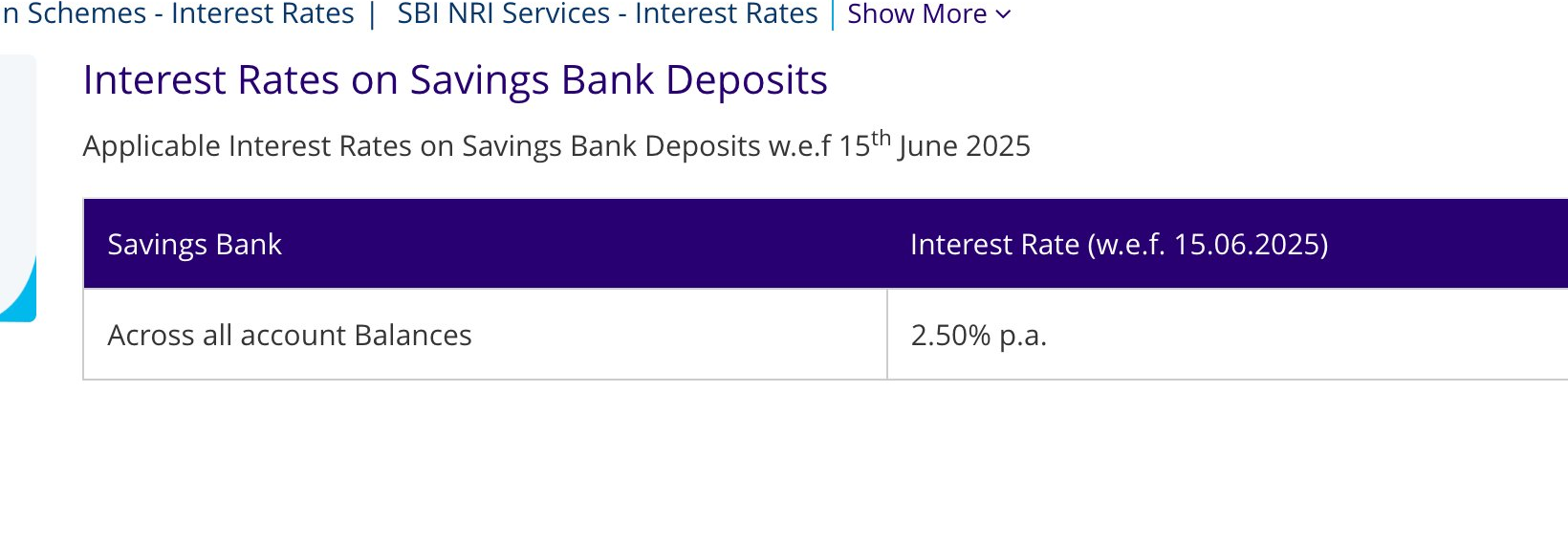

📊Interest Rates on Savings Account - Both Now at 2.50%

Both SBI and HDFC currently offer 2.50% per annum on savings account deposits across all balance slabs. This is a major change from earlier years when HDFC offered 3.00% and SBI 2.70%.

SBI cut its rate to 2.50% with effect from 15 June 2025. HDFC followed with a cut to 2.50% effective 24 June 2025.

Interest is no longer a differentiator between SBI and HDFC for savings accounts. If you are choosing between these two banks purely for higher returns, neither has an edge anymore.

For better savings interest, smaller private banks like RBL, IDFC First, or Bandhan still offer 3.50%-6.00%. Small finance banks like AU Small Finance Bank or Equitas offer up to 7.00%-7.50%.

The real decision between SBI and HDFC now hinges on minimum balance requirements, quarterly charges, branch network, and digital banking experience - not interest rate.

HDFC Savings Account Rate Cuts Timeline

| Period | Below ₹50 Lakh | ₹50 Lakh - ₹500 Cr |

|---|---|---|

| April 2022 - April 2025 | 3.00% | 3.50% |

| 12 April 2025 - 9 June 2025 | 2.75% | 3.25% |

| 10 June 2025 - 23 June 2025 | 2.75% | 2.75% |

| 24 June 2025 onwards | 2.50% | 2.50% |

💳Minimum Balance Requirements - A Critical Difference

Minimum balance requirements impact your effective returns because penalties for non-maintenance eat into your interest income. Here is how SBI and HDFC Bank compare:

SBI: Minimum balance requirements vary by branch type. Metro/Urban branches: ₹3,000.

Semi-urban branches: ₹2,000. Rural branches: ₹1,000.

SBI has significantly reduced penalties for non-maintenance - the maximum penalty is ₹10-15 per month, and basic savings accounts (BSBD accounts) have zero minimum balance requirements.

HDFC BANK: Regular savings account minimum balance is ₹10,000 in metro/urban branches and ₹5,000 in semi-urban/rural branches. Non-maintenance charges range from ₹150-600 per quarter depending on the shortfall amount.

HDFC Bank's basic savings account (no minimum balance) has limited features - only 4 ATM transactions per month and no cheque book.

For students, salaried employees, and budget-conscious individuals, SBI's lower minimum balance requirements are a significant advantage. HDFC Bank's ₹10,000 requirement means ₹10,000 of your money is essentially locked up just to avoid penalties - that is money you cannot use for expenses or investments.

PRACTICAL TIP: If you choose HDFC Bank, ask for a salary account through your employer. HDFC salary accounts have zero minimum balance requirements, and most medium-to-large companies have salary account tie-ups with HDFC Bank.

Real Cost of HDFC Low Balance: ₹600 to ₹2,400 per Year

💡Real Cost of HDFC Low Balance: ₹600 to ₹2,400 per Year

If you regularly drop below ₹10,000 in your HDFC metro account, the quarterly non-maintenance charges are calculated as 6% of the shortfall, capped at ₹600 per quarter. In the worst case you pay ₹2,400 per year just in penalties - more than the ₹250 annual interest you would earn on a ₹10,000 balance at 2.50%.

SBI has zero such charges, so cost-conscious savers come out ahead with SBI by ₹2,400-3,000 per year.

📱Digital Banking Experience - HDFC Bank Leads

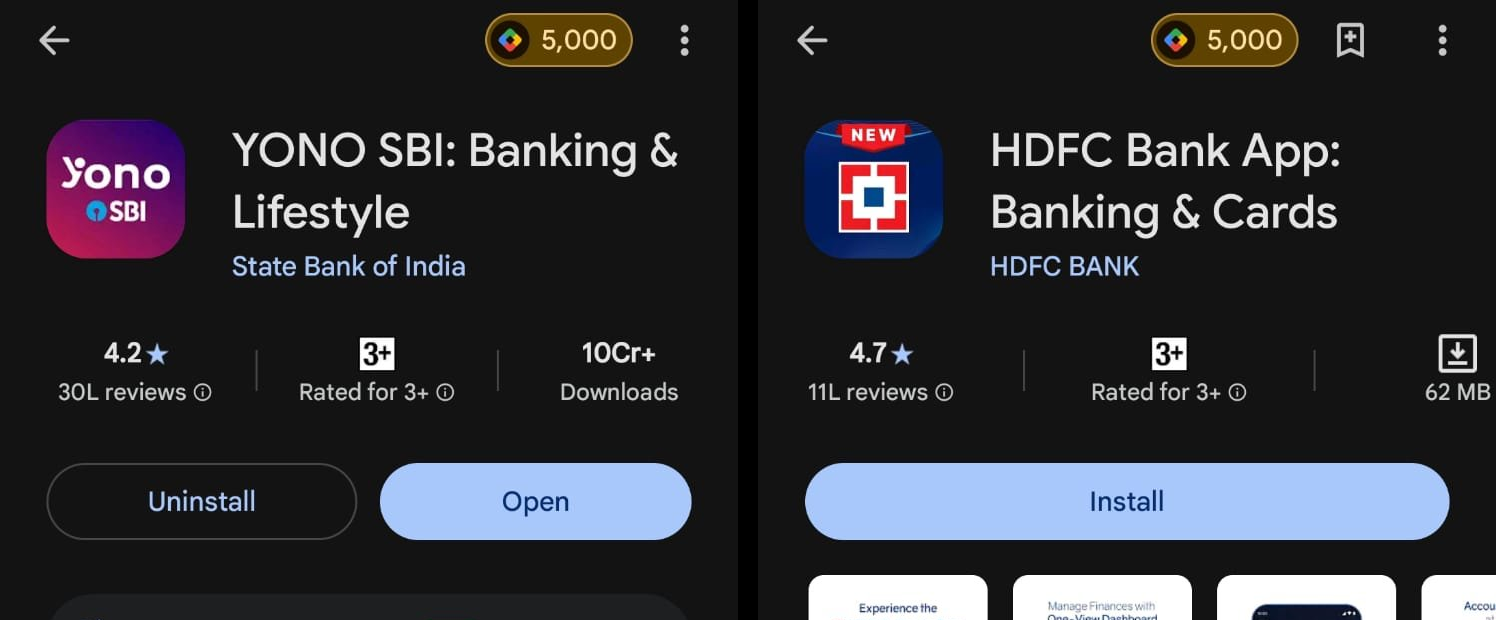

In terms of digital banking, HDFC Bank has a clear advantage with its PayZapp and HDFC Bank Mobile Banking app, which consistently rank among the best banking apps in India. Features include instant fund transfers (UPI, IMPS, NEFT, RTGS), bill payments, credit card management, investment products, and a smooth user interface.

SBI's YONO (You Only Need One) app has improved dramatically in recent years and now offers a comprehensive digital banking experience. YONO provides savings account management, UPI payments, mutual fund investments, insurance, loan applications, and even e-commerce shopping.

However, users frequently report slower response times, server issues during peak hours, and occasional crashes compared to HDFC Bank's app.

For internet banking, HDFC Bank's NetBanking platform is more intuitive and faster than SBI's OnlineSBI. HDFC Bank also offers better integration with third-party apps, payment gateways, and financial tools.

SBI's internet banking has all the essential features but the interface feels dated and navigation can be clunky.

That said, SBI's YONO has one major advantage - its user base. With 60+ crore accounts, SBI's digital infrastructure handles massive scale, and the UPI payment success rate has improved to match private banks.

For basic banking needs - checking balance, transferring money, paying bills - both apps work well enough.

🏦Branch and ATM Network - SBI Dominates

SBI has the largest branch and ATM network in India by a massive margin. SBI operates 22,000+ branches and 65,000+ ATMs across the country, including in the remotest towns and villages where no private bank has a presence.

If you live in or frequently travel to rural or semi-urban India, SBI is the only bank that guarantees you will find a branch or ATM nearby.

HDFC Bank has approximately 8,000+ branches and 20,000+ ATMs, primarily concentrated in urban and semi-urban areas. In metro cities, HDFC Bank's branch density is comparable to SBI.

But in rural India, tier-3 towns, and border areas, HDFC Bank's presence drops sharply.

Free ATM transaction limits: SBI provides 5 free transactions per month at SBI ATMs and 3 at other bank ATMs. After that, ₹20 per transaction (+ GST) is charged.

HDFC Bank provides 5 free transactions at HDFC ATMs in metro cities (unlimited in non-metro) and 3 at other bank ATMs.

For government employees, defence personnel, and people posted in remote areas, SBI's extensive network is a decisive advantage. HDFC Bank is primarily an urban bank - excellent in cities, limited in the hinterland.

SBI vs HDFC At a Glance - Key Numbers 2026

2.50%

Interest (Both)

22,000+

SBI Branches

4.7★

HDFC App Rating

₹5 Lakh

DICGC Insurance

🏛️Government Services and Scheme Integration

SBI, as the largest public sector bank, is the default banking partner for most government schemes and services. If you receive any government benefits - LPG subsidy (DBTL), PM-KISAN, MGNREGA wages, pension, scholarships, or any Direct Benefit Transfer - SBI accounts ensure the smoothest processing with fewest glitches.

Government salary accounts for central and state government employees are predominantly with SBI. Defence salary accounts, railway employee accounts, and PSU salary accounts are typically with SBI.

If you are a government employee, having an SBI account simplifies everything - your salary, GPF, loans, and benefits all flow through one bank.

HDFC Bank is popular for salary accounts in the private sector. Most MNCs, tech companies, and large private employers have salary account tie-ups with HDFC Bank, ICICI Bank, or Axis Bank.

If you work in the private sector, your employer's salary account bank may not give you a choice - and HDFC Bank salary accounts are among the best in terms of features and service.

For linking with government portals like DigiLocker, UMANG, Income Tax e-filing, and GST portal, both SBI and HDFC Bank work seamlessly. The integration advantage of SBI is primarily for receiving government benefit transfers.

SBI Scale Advantage - Why Government Trusts SBI

50+ Cr

SBI Accounts

57.49%

Govt Stake

11,500+

Rural Branches

1955

Established

💰Loan Products - Interest Rates and Processing

For home loans, SBI typically offers the lowest interest rates in the market - currently starting at 8.50% (linked to EBLR). HDFC Bank's home loan rates start at 8.75%.

On a ₹30 lakh home loan over 20 years, SBI's 0.25% lower rate saves approximately ₹1.5-2 lakh over the loan tenure. SBI also offers special rates for women borrowers (0.05% concession).

For personal loans, HDFC Bank has faster processing (disbursement within 10 seconds for pre-approved customers) but higher interest rates (10.75-21.00%). SBI personal loans are cheaper (11.00-14.30%) but processing takes 2-7 days.

For education loans, SBI's interest rates (8.15-10.65%) are among the lowest, and SBI is the largest education loan provider in India.

Car loans, gold loans, and business loans are competitive at both banks. The general pattern holds - SBI offers lower rates with slower processing, while HDFC Bank offers slightly higher rates with faster, more convenient processing.

If you plan to take any loan in the next 5 years, maintaining a good relationship with your bank (healthy savings balance, timely bill payments) helps in getting pre-approved offers at competitive rates. Both banks use your transaction history to determine credit offers.

✅Our Recommendation - Who Should Choose Which Bank (Updated for 2026)

Since both banks now offer the same 2.50% interest, the choice depends entirely on your balance, location, and digital habits.

Choose SBI if you maintain low balances, live in a non-metro area, work with government services, or want zero balance penalties. SBI has no minimum balance for regular accounts, and its branch network reaches every district.

Choose HDFC if you can comfortably maintain ₹10,000 in metros (or ₹5,000 semi-urban), prefer modern app banking, and value faster customer service. HDFC's app rating (4.7★) significantly beats YONO SBI (4.2★).

Avoid HDFC if your salary or business income fluctuates and you might drop below the ₹10,000 metro balance, since quarterly non-maintenance charges of ₹150-600 will eat into any interest gains.

Hybrid strategy: Many financially aware Indians use SBI as their primary salary/savings account (zero risk) and HDFC as a secondary account for credit cards and digital banking. This is now even more attractive since interest is equal.

📞Customer Service and Grievance Resolution

Customer service quality is where private banks like HDFC Bank traditionally outperform public sector banks like SBI. HDFC Bank offers 24x7 phone banking with shorter wait times (typically 2-5 minutes), dedicated relationship managers for premium customers, and responsive social media support on Twitter and Facebook.

SBI's customer service has improved significantly with the YONO app and toll-free number (1800-1121), but branch-level service remains inconsistent. In metro branches with heavy footfall, wait times of 30-60 minutes for basic transactions are common.

SBI's complaint resolution timelines are longer - typically 15-30 days versus 7-15 days at HDFC Bank.

For grievance escalation, both banks follow RBI's Integrated Ombudsman Scheme. If your complaint is not resolved within 30 days by the bank, you can escalate to RBI's Banking Ombudsman at cms.rbi.org.in.

The ombudsman can order compensation up to ₹20 lakh for deficiency in service.

One area where SBI has improved dramatically is UPI complaint resolution. SBI now resolves most UPI transaction failures within 48 hours automatically, compared to the 5-7 day timelines of a few years ago.

For day-to-day digital transactions, the service gap between SBI and HDFC Bank has narrowed considerably.

🔒Safety and Deposit Insurance - Both Are Safe

Both SBI and HDFC Bank are safe for your deposits. All bank deposits in India are insured up to ₹5 lakh per depositor per bank by DICGC (Deposit Insurance and Credit Guarantee Corporation), a subsidiary of RBI.

This ₹5 lakh limit covers savings accounts, fixed deposits, current accounts, and recurring deposits combined.

SBI carries additional implicit safety as a government-owned bank. The Government of India holds a majority stake in SBI (approximately 57.5%), and there is an implicit sovereign guarantee - the government would not allow SBI to fail.

This makes SBI deposits effectively risk-free regardless of the ₹5 lakh DICGC limit.

HDFC Bank, as a private sector bank, is regulated by the same RBI norms and must maintain the same Capital Adequacy Ratio (CAR) as public sector banks. HDFC Bank's CAR is typically higher than the regulatory minimum (19-20% vs required 11.5%), indicating strong financial health.

The risk of a top-3 private bank like HDFC Bank failing is extremely low.

PRACTICAL ADVICE: If you have more than ₹5 lakh in savings, spread your deposits across multiple banks to maximize DICGC coverage. Keep ₹5 lakh at SBI and ₹5 lakh at HDFC Bank - this way, ₹10 lakh is fully insured.

For amounts above this, consider fixed deposits at different banks or invest in government securities (G-Secs) through RBI Retail Direct for absolute safety.

Both Banks Are 100% Safe - DICGC Insures ₹5 Lakh Each

💡Both Banks Are 100% Safe - DICGC Insures ₹5 Lakh Each

Both SBI and HDFC are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a wholly-owned subsidiary of the RBI. Each depositor is insured up to ₹5 lakh per bank for the combined value of savings, current, fixed deposit, and recurring deposit accounts.

If you have ₹5 lakh in SBI and another ₹5 lakh in HDFC, you are fully insured for ₹10 lakh total. SBI carries an additional implicit guarantee from being majority government-owned (57.49% Government of India stake).

The smart move for most people

💡The smart move for most people

Keep your salary account where your employer mandates (usually HDFC/ICICI for private sector). Open a secondary SBI BSBD account for zero-balance emergency savings.

Use HDFC for daily transactions and UPI, SBI for government subsidy credits and rural accessibility.

On ₹1 lakh balance, HDFC pays ₹3,000/year interest vs SBI's ₹2,700. That ₹300 difference is real - but if you miss maintaining HDFC's ₹10,000 minimum balance even once, the ₹600 quarterly penalty wipes out the entire interest advantage.

🏦Choose SBI If...

You Need Zero Minimum Balance

SBI Basic Savings Bank Deposit (BSBD) account has ₹0 minimum balance and ₹0 charges. HDFC's basic account still requires ₹2,500 minimum.

For students, low-income families, migrant workers, or Jan Dhan beneficiaries, SBI is the clear choice. You can keep a ₹0 balance account open permanently without penalties.

You Live in Rural or Semi-Urban India

SBI has 22,000+ branches - almost every block in India has an SBI branch. HDFC has limited rural presence (concentrated in metros and tier-1 cities).

If your village is 100 km from the nearest HDFC branch, SBI makes practical sense. Government benefits (pension, PM Kisan) are also primarily disbursed through SBI in rural areas.

You Receive Government DBT Payments

🏦More Reasons to Choose SBI

PM Kisan subsidy, NREGA wages, scholarships, pensions, and LPG subsidies flow through SBI most smoothly. SBI's integration with government payment systems is unmatched.

If you depend on government benefits, SBI ensures smooth, timely receipt.

You Want the Safest Bank

SBI is government-owned (after 2008 reforms, government still holds 59.7% stake). This provides an implicit sovereign guarantee - SBI can never be allowed to fail by the Indian government.

While HDFC is the largest private bank in India and equally safe, SBI has a unique government backing that some customers prefer for peace of mind.

You Don't Use Banking Apps

If you prefer visiting branches for transactions or don't do online banking, SBI's widespread branch network is invaluable. HDFC's focus on digital banking means branch service is not prioritized - you may face longer waits.

🏦Choose HDFC If...

You Want the Best Digital Experience

HDFC's mobile banking app is consistently rated the best among Indian banks. Faster, more features, intuitive UI, and quicker approvals for loans/credit cards.

If you do 90% of banking on your phone, HDFC wins decisively. SBI YONO is improving but still lags behind HDFC's app.

You Can Maintain ₹10,000 Minimum Balance

If ₹10,000 sitting in savings doesn't bother you (because you already have that much cash reserve), HDFC's higher interest rate (3.25% vs 2.70%), better digital banking, and superior customer service justify the higher minimum. Over a year, the 0.55% extra interest on ₹10,000 = ₹55 extra.

Plus non-maintenance fee avoided.

You Want Premium Banking and Credit Cards

HDFC's credit card ecosystem is unmatched. HDFC Millennia card (₹500/year): highest everyday rewards among peer cards.

Regalia (₹2,500/year): airport lounge access, concierge service. Infinia (₹5,000/year): ultra-premium with exceptional benefits.

SBI's SimplyCLICK and Elite cards are decent but a tier below HDFC's offerings.

You're in a Metro City

HDFC branches in metros are better maintained, less crowded, and faster than SBI. In Tier-1 cities, the service and experience difference in HDFC branches is noticeable and better.

If you occasionally need branch visits, HDFC is superior in metros.

You Want Integrated Wealth Management

HDFC offers investment advisory, mutual funds, insurance, and wealth management services seamlessly integrated with your savings account. SBI's services are more fragmented.

If you're planning to invest through your bank, HDFC is more convenient.

🔀Hybrid Approach: Why Have Both?

Many financially savvy Indians maintain accounts in both banks:

Dual Account Strategy

Primary account: SBI for receiving government DBT payments, pension (if applicable), and payroll (if government employee). Secondary account: HDFC for daily transactions, bill payments, investments, and credit card payments.

This maximizes benefits of both: SBI's government integration + HDFC's digital convenience. Money flows from SBI → HDFC as needed.

Interest Arbitrage

Keep high balance in HDFC (3.25% interest) for the month. Few days before interest is credited, transfer excess to SBI FD (higher rate, 7.1% vs HDFC 7.0%).

This is interest optimization for people with ₹1L+ in savings. Small benefit but adds up over years.

Fee Minimization

Keep minimum balance in SBI only (₹1,000 to avoid penalty). Keep optimized balance in HDFC (₹10,000+) where interest and services are better.

This hybrid approach minimizes fees while optimizing returns.

Digital Banking - Which Bank App Wins in 2026

4.7★

HDFC App Rating

4.2★

YONO SBI Rating

₹1 Lakh

UPI Limit

24x7

Net Banking

💼Salary Account - SBI or HDFC for Working Professionals?

For salary accounts, the calculation flips slightly in HDFC's favor because most salary accounts are zero-balance and avoid the ₹10,000 minimum balance penalty.

HDFC offers Classic, Regular, Premium, and Imperia salary account tiers based on your monthly salary credit (₹25,000 to ₹10 lakh+). Higher tiers come with free debit cards, lounge access, and dedicated relationship managers.

SBI Corporate Salary Account is also zero-balance with no quarterly charges. It works well for government employees, PSU staff, and traditional companies.

Comes with free ATM cards and personal accident insurance up to ₹20 lakh for higher tiers.

Verdict for salary account: HDFC wins for private sector professionals who value app banking, faster grievance resolution, and travel perks. SBI wins for government/PSU employees, those in tier-2/3 cities, and anyone wanting maximum security with widest branch coverage.

Important: Once you leave the company, salary accounts convert to regular savings accounts after 3-6 months. At that point HDFC's ₹10,000 minimum balance kicks in (with ₹150-600 quarterly charges if not maintained).

Plan accordingly.

How to Switch from HDFC to SBI (or Vice Versa)

❓Frequently Asked Questions

📋 Official Sources & Verification

Information verified against official government portals and gazette notifications. Read our editorial process.

June 2026