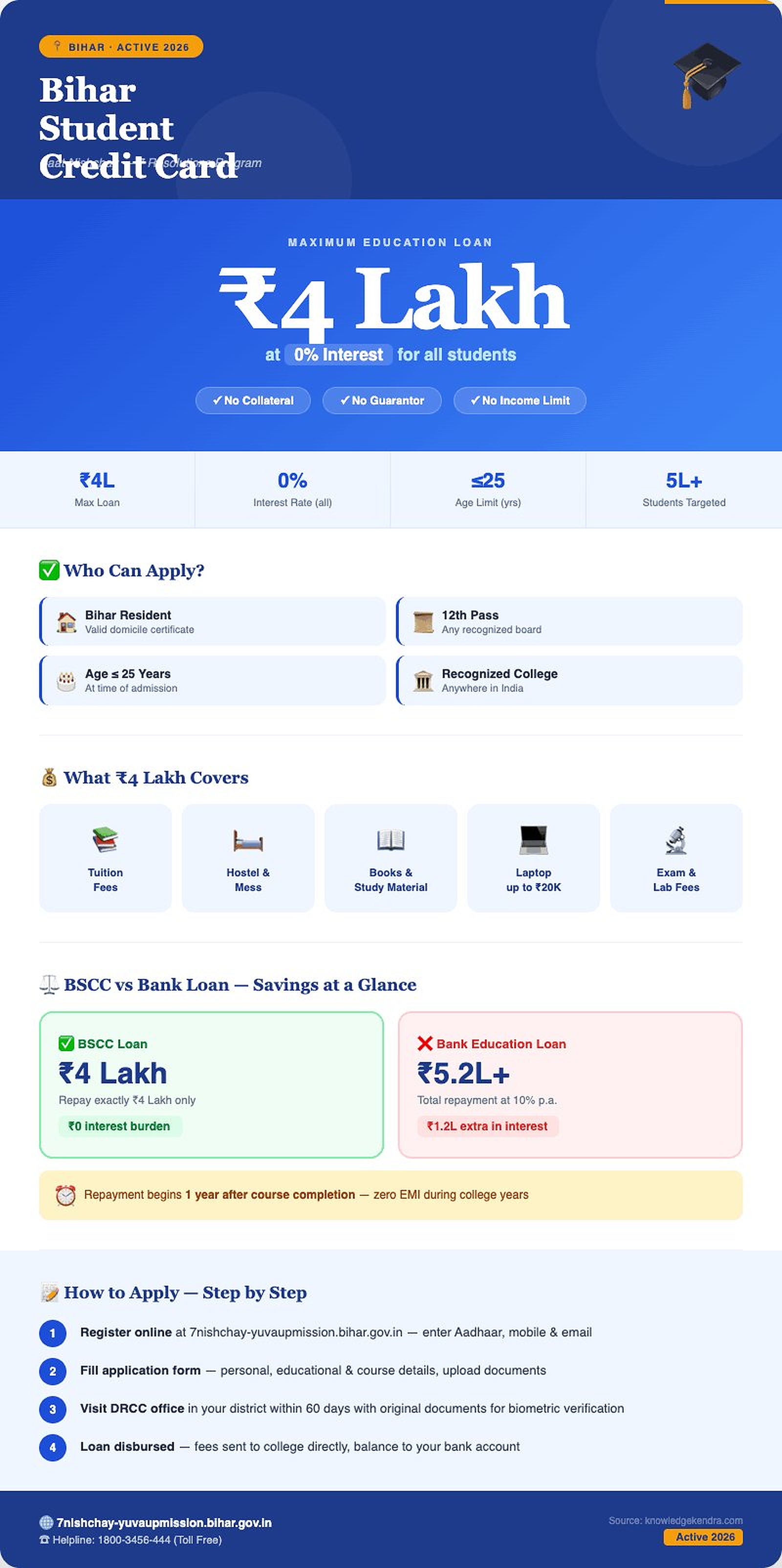

Bihar Student Credit Card 2026 - ₹4 Lakh DRCC Loan Guide: Bihar gives up to Rs 4 lakh education loan for higher studies. Loans sanctioned from September 2025 carry 0% interest. Earlier loans were 4% general and 1% for women, transgender and Divyang students..Loan Amount: Up to ₹4 Lakh. Interest Rate: 0% (new) / 4% old. Target: 5 Lakh+ Students. Repayment: After course + 1yr.Bihar Student Credit Card (BSCC) is a transformational education financing scheme under the '7 Nishchay' (Seven Resolutions) program of the Bihar government. It provides education loans up to ₹4 lakh to 12th pass students at ZERO interest - a historic rate reduction from the earlier 1-4% regime.

On This Page

Active SchemeUpdated: May 2026

🎓

Bihar Student Credit Card 2026 - ₹4 Lakh DRCC Loan Guide

Bihar gives up to Rs 4 lakh education loan for higher studies. Loans sanctioned from September 2025 carry 0% interest. Earlier loans were 4% general and 1% for women, transgender and Divyang students.

Loan Amount

Up to ₹4 Lakh

Interest Rate

0% (new) / 4% old

Target

5 Lakh+ Students

Repayment

After course + 1yr

📖What is Bihar Student Credit Card 2026 - ₹4 Lakh DRCC Loan Guide?

Bihar Student Credit Card (BSCC) is a transformational education financing scheme under the '7 Nishchay' (Seven Resolutions) program of the Bihar government. It provides education loans up to ₹4 lakh to 12th pass students at ZERO interest - a historic rate reduction from the earlier 1-4% regime.

The scheme covers all courses at recognized institutions across India and has zero collateral, zero guarantor requirements, making it the most accessible higher education loan in India.

As per the Chief Minister's announcement in 2024-2025, the interest rate was slashed to 0% for ALL students (previously differentiated: 0% for girls/transgender/disabled, 1% for boys). This universalization reflects Bihar's commitment to making higher education affordable.

The loan covers legitimate education expenses: tuition fees, examination fees, hostel accommodation, library fees, books and study materials, laptop/tablet purchase (up to ₹20,000), and other institutional charges.

The scheme is revolutionary for economically weaker sections: unlike commercial bank education loans (8-12% interest with collateral requirements), BSCC requires NO collateral, NO guarantor, and has 0% interest. For a ₹4 lakh loan, a student repays exactly ₹4 lakh (no interest accumulation).

Repayment starts AFTER course completion + 1 year grace period - meaning zero payments during 3-4 year college years. An engineering student borrowing ₹4 lakh pays back ₹333/month for 10 years post-graduation, vs. ₹10,000+/month for bank loans.

As of March 2026, over 3.5 lakh students have availed BSCC loans across engineering, medical, management, arts, science, and vocational courses. Total disbursements: ₹14,000+ crore.

The scheme has been particularly impactful in rural Bihar where college education was previously financially inaccessible to 80% of families.

✅Eligibility

Bihar ResidenceMust be permanent resident of Bihar. Aadhaar with Bihar address or domicile certificate acceptable.

Education QualificationMust have passed 12th (10+2) from any recognized board (CBSE, ICSE, State Board). No minimum percentage cutoff.

Age LimitMust not exceed 25 years at time of application. A 26-year-old returning to studies is ineligible.

Course RequirementsMust be pursuing or have admission in a recognized degree/diploma course (42+ courses covered: B.Tech, MBBS, BA, BSc, BCom, BBA, LLB, BCA, MA, MSc, MBA, MCA, BFA, etc.). Duration must be minimum 1 year (masters), 2 years (graduation), or 4 years (engineering).

Family IncomeNo strict ceiling, but scheme targets economically weaker families. As guideline: annual family income should not exceed ₹5 lakh. However, students from higher income families also approved if pursuing loan.

Loan LimitActual tuition fee charged by institution OR ₹4 lakh (whichever is LOWER). Covers fees + hostel + books + laptop. Total cannot exceed ₹4 lakh.

Interest RateZERO percent (0%) for ALL students (males, females, transgender, disabled). Recently universalized from earlier differentiated rates.

Debt ObligationYou repay exactly what you borrow - ₹1 lakh loan → ₹1 lakh repayment. Zero interest means no financial burden beyond principal.

✅

Not sure if you qualify?

Check your eligibility for 50+ government schemes in 2 minutes. No login, no fees. Just answer a few simple questions.

💰Covered Expenses - What ₹4 Lakh Loan Can Pay For

| Expense Category | Amount Covered | Notes |

|---|---|---|

| Tuition/College Fees | As charged by institution | For recognized college/university only |

| Examination Fees | Actual cost per semester | Including internal, practical, final exam fees |

| Hostel/Accommodation | Actual hostel rent/charges | If living away from home |

| Library Fees | ₹1,000-3,000/year | As per institution's library subscription |

| Lab/Practical Fees | Actual cost | Engineering/science practicals |

| Books and Stationery | Actual cost (limit ₹10K) | Essential textbooks and study materials |

| Laptop/Tablet | Up to ₹20,000 | One-time for academic use only |

| Development Charges | Actual amount charged | Infrastructure fee, sports fee, etc. |

| Online Course Materials | ₹2,000-5,000 | For distance learning or online components |

| Skill Certification Exam | ₹5,000-10,000 | If part of course curriculum |

₹4 Lakh

Maximum loan

0% new / 4%-1% old

Interest general/women

5 Lakh+

Target students

Age 25

Upper age limit

⚖️BSCC vs Bank Education Loans - Why BSCC Wins

BSCC: 0% interest on loans sanctioned from September 2025, zero collateral, zero guarantor, starts repayment after 1-year grace. For ₹4L loan: repay ₹4L over 10 years = ₹333/month.

Net cost: ₹4L (nothing extra).

Bank Loan (SBI/HDFC): 8-12% interest, requires collateral (land/property worth ₹10L+), requires guarantor, immediate EMI pressure post-disbursement. For ₹4L loan at 10% p.a.: total repayment ₹5.2L+ over 10 years = ₹434/month.

Net cost: ₹5.2L+ (1.2L+ extra as interest).

Private Finance Company: 15-18% interest, strict collateral requirements, 100% of amount loaned, sometimes predatory terms. For ₹4L: total repayment ₹6.5L+ over 10 years = ₹542/month.

Net cost: ₹6.5L+ (extra ₹2.5L as interest).

Ground reality: Most banks reject education loans for students from poor background (no collateral). BSCC is the ONLY option for 80% of rural Bihar's eligible students.

This financial inclusion is the scheme's strongest impact.

📖Real Example - How BSCC Changed a Student's Life

Meet Anjali: 18 years old, from Madhubani, Bihar. Passed 12th with 65% marks from a government school.

Parents are small farmers (annual income ₹2.5 lakh). Had admission in B.Tech program at NIT Patna (₹3.5L total 4-year cost).

Without BSCC: Parents couldn't afford NIT fees. Anjali's only options: local govt college (free) OR work at age 18.

She'd lose opportunity for national-level education. IIT/NIT dream crushed.

With BSCC: Applied at 7nishchay portal. Submitted 12th mark sheet, Aadhaar, domicile, bank account, NIT admission letter.

Visited DRCC in Madhubani district with original documents. DRCC verified and approved ₹3.5L loan within 45 days.

NIT fees paid from loan, Anjali studied tension-free.

Outcome: Anjali completed B.Tech. Got ₹8L salary job at TCS.

Started repaying ₹23K/month. Loan will be cleared in 15 months (she's overpaying to close quickly).

Parents' farm now has solar pump (Anjali bought it post-job). Entire family's socioeconomic trajectory changed due to BSCC.

₹4 Lakh

Maximum loan under Bihar Student Credit Card

BSCC provides up to ₹4 lakh collateral-free education loan to Bihar residents who have passed Class 12. Covers tuition, books, laptop, accommodation for courses across India.

🏛️DRCC (District Registration Counseling Center) - The Make-or-Break Step

DRCC is the district-level office where document verification happens. This is THE most critical step - your entire loan depends on DRCC approval.

Locations: Usually at District Magistrate office or district education board office.

What DRCC checks: (1) Aadhaar-based identity verification, (2) 12th mark sheet authenticity (cross-check with board), (3) Domicile certificate authenticity, (4) Bank account validity (will they accept BSCC transfers?), (5) Admission letter authenticity (contact college to verify), (6) Family income (scrutinize ITR or income certificate).

Timeline: Visit DRCC within 60 days of online application. If delayed, application may be rejected and reapplication required.

DRCC visits are typically on weekdays 10 AM - 5 PM. Bring ALL original documents + 2 copies.

Processing: 30-60 days after DRCC visit.

Common DRCC rejections: (1) Aadhaar spelling doesn't match 12th mark sheet (name 'Asha' in Aadhaar, 'Ashar' in school records), (2) Admission letter is fake or college is unrecognized, (3) Income certificate is too old (>6 months), (4) Bank account is in someone else's name. Before DRCC visit, get all documents cross-verified for consistency.

🎓What is Bihar Student Credit Card scheme?

Bihar Student Credit Card (BSCC) launched in October 2016 by the Bihar state government is one of India's most progressive education financing schemes. It provides loans up to Rs 4 lakh at just 4% simple interest (1% for women, transgender, and disabled students) for higher education - covering tuition fees, hostel, books, laptop, and other academic expenses.

No collateral, no guarantor, no bank visit required.

The scheme was born from a stark reality: Bihar has the lowest Gross Enrollment Ratio (GER) in higher education among major states - approximately 15% vs the national average of 28%. Lakhs of 12th-pass Bihar students couldn't afford college fees, even for courses costing Rs 20,000-50,000/year.

The Rs 4 lakh credit card, now at 0% interest for loans sanctioned from September 2025, removes the financial barrier completely.

Unlike bank education loans (which require collateral for amounts above Rs 4 lakh, charge 8-12% interest, and involve complex documentation), BSCC is processed entirely by the state education department - not banks. You apply online, submit documents at the district DRCC (District Registration and Counselling Centre), and receive funds directly.

The simplicity of the process is what makes this scheme transformative.

📋Who is eligible?

Domicile: Must be a permanent resident of Bihar. Domicile certificate or residential certificate from the district is required.

Students born in Bihar who moved to other states for schooling can apply if they have Bihar domicile.

Education: Must have passed 12th class (intermediate) from a recognized board - BSEB (Bihar Board), CBSE, ICSE, or any state board. The loan covers higher education: graduation (BA, BSc, BCom, BBA, BCA), professional courses (BTech, MBBS, BDS, LLB, BPharm), diploma, polytechnic, and recognized vocational courses.

The institution can be in Bihar or any other state in India.

Age: No specific age limit mentioned for the scheme - but since it's for students progressing from 12th to higher education, the practical age range is 17-25. There's no maximum age cutoff explicitly stated, so mature students returning to education may also apply.

Income: No income ceiling. Unlike most government schemes that cap family income at Rs 2-8 lakh, BSCC has NO income limit.

A Bihar student from a family earning Rs 15 lakh/year is equally eligible as one from a family earning Rs 1 lakh/year. This universal eligibility is rare among education financing schemes and eliminates the need for income certificates.

BSCC Age Limit, Domicile, 12th Pass Requirements

Age limit: must not exceed 25 years on date of admission (relaxation for SC/ST/Divyang). Domicile: permanent Bihar resident with valid certificate.

Educational qualification: Class 12 passed.

📝How to apply - step by step

Step 1: Visit the official portal at 7nishchay-yuvaupmission.bihar.gov.in. Click on 'Student Credit Card' → New Registration.

Enter your Aadhaar number, mobile number, and email. OTP verification on both mobile and email.

Step 2: Fill the online application form - personal details (name, DOB, address, parents' details), educational details (12th board, marks, year of passing), course details (which course you want to study, at which institution, expected fees), and bank account details (your personal savings account for loan disbursement).

Step 3: Upload documents - Aadhaar card, 10th and 12th marksheets, admission letter or bonafide certificate from the institution, fee structure from the institution, Bihar domicile/residential certificate, passport-sized photo and signature. All uploads as PDF/JPEG under 500 KB each.

Step 4: After online submission, you receive an appointment date to visit your district's DRCC (District Registration and Counselling Centre). Visit the DRCC with original documents for verification.

The DRCC officer verifies your identity, education certificates, and admission details. This visit takes 30-60 minutes.

Step 5: After DRCC verification, the application is forwarded to the loan-disbursing bank (channelized by the state government - typically IDBI Bank or other designated banks). Loan sanctioned within 15-30 days of DRCC visit.

Funds transferred to your bank account in installments - typically semester-wise or yearly based on the fee schedule you submitted.

How to Login at 7nishchay-yuvaupmission.bihar.gov.in

1

Visit Portal

Open 7nishchay-yuvaupmission.bihar.gov.in

2

Click Login

Enter credentials from registration SMS

3

Verify OTP

OTP to Aadhaar-linked mobile

4

Dashboard

View status, upload docs, track verification

💰What expenses does the Rs 4 lakh cover?

Tuition fees: The primary expense covered - whatever your institution charges as tuition. For Bihar government colleges, tuition is Rs 5,000-20,000/year.

For private engineering colleges, it's Rs 50,000-1,50,000/year. For medical colleges, it can be Rs 1-5 lakh/year.

The Rs 4 lakh limit covers most government and affordable private institutions for 3-4 year courses.

Hostel and mess charges: If you're studying outside your hometown, hostel fees and mess (food) charges are covered. For students going to institutions in other states (Delhi, Pune, Bangalore), hostel costs of Rs 30,000-80,000/year are a significant expense that the credit card helps with.

Books, stationery, and study material: Textbooks for engineering, medical, and law courses cost Rs 5,000-15,000/year. Lab equipment, drawing instruments, and other course-specific materials are also covered.

Keep receipts - the loan account tracks utilization.

Laptop/computer: Up to Rs 35,000 for purchasing a laptop - essential for engineering, IT, management, and most modern courses. The laptop cost is part of the Rs 4 lakh total limit, not additional.

Buy within the first year of the course - some students wait and then can't claim because the remaining loan balance is too low.

Living expenses: A portion of the Rs 4 lakh can cover daily living expenses during the course - food, transport, stationery, internet. However, the scheme doesn't separately categorize 'living allowance' - the total Rs 4 lakh must cover ALL expenses.

Budget carefully to ensure the money lasts the entire course duration.

Quick BSCC Eligibility Check

You qualify if

- Permanent resident of Bihar

- Passed Class 12 from recognised board

- Age 25 or below at admission

- Admitted to recognised institution

- Course listed under approved BSCC streams

- Aadhaar linked to mobile

You won't qualify if

- Above 25 years at admission

- Not a Bihar domicile

- Already availed BSCC

- Institution not accredited

- Short-duration certificate course

- Defaulted on prior government loan

🔄Repayment - when and how

Moratorium period: You don't start repaying during the course. Repayment begins 12 months after course completion - giving you time to find a job.

If your course is 4 years (BTech), the moratorium period effectively gives you 5 years before the first EMI is due. This is more generous than most bank education loans which start interest accrual during the course.

For loans from September 2025, interest is 0%, so you repay only the principal.

Interest rate: 4% simple interest for male students. 1% simple interest for women, transgender, and disabled students.

On Rs 4 lakh loan at 4%: annual interest is Rs 16,000, total interest over a 4-year course + 1-year moratorium = Rs 80,000.

Total repayment: Rs 4,80,000 spread over the repayment period. For women at 1%: total interest over 5 years = Rs 20,000.

Total repayment: Rs 4,20,000.

Repayment period: Up to 84 months (7 years) to repay after the moratorium period ends. Monthly EMI on Rs 4 lakh at 4% over 7 years: approximately Rs 5,700/month.

At 1% (women): approximately Rs 5,000/month. These EMIs are manageable for most graduates earning Rs 15,000-30,000/month.

What if you can't repay? The Bihar government has introduced a loan waiver provision for students who complete their course but remain unemployed for 2 years after the moratorium period.

The specific conditions for waiver are updated periodically - check the 7nishchay portal for current waiver eligibility. Don't default without exploring the waiver option - defaulting affects your CIBIL score even on government-channelized loans.

⚖️BSCC vs bank education loan vs Vidyalakshmi

BSCC advantage: 4% interest (vs 8-12% bank loans), no collateral (banks require collateral above Rs 4 lakh), no income proof needed (banks assess parents' income), simple state government process (vs complex bank documentation). For Bihar students, BSCC is almost always better than a bank education loan for amounts up to Rs 4 lakh.

Bank education loan advantage: Higher amount - up to Rs 10 lakh (without collateral) and Rs 20 lakh+ (with collateral). Covers expensive courses like MBA at IIMs (Rs 20-25 lakh), MBBS at private medical colleges (Rs 50 lakh+), and foreign education (Rs 1 crore+).

If your course costs more than Rs 4 lakh, you'll need a bank loan - BSCC's Rs 4 lakh limit won't cover expensive private institutions.

Can you get both? If your total education cost is Rs 8 lakh: take Rs 4 lakh from BSCC (at 4% interest) and Rs 4 lakh from bank education loan (at 8-10% interest via Vidyalakshmi portal).

This hybrid approach minimizes your total interest cost. The BSCC and bank loan are independent - one doesn't affect the other.

Vidyalakshmi portal (vidyalakshmi.co.in): Central government portal for education loans from multiple banks. If you need more than Rs 4 lakh or want to apply to banks alongside BSCC, use Vidyalakshmi.

One application reaches multiple banks. Apply for BSCC first (lower interest), then supplement with Vidyalakshmi if BSCC doesn't cover your total cost.

BSCC vs DRCC vs Bihar Education Loan - Same Scheme

BSCC is the official scheme name. DRCC is the office where you apply.

Bihar Education Loan is the generic term. All refer to the same ₹4 lakh scheme launched 2016 under Mukhyamantri Nishchay Yojana.

🎓Approved Colleges and Courses Under BSCC

BSCC covers degree, diploma, and professional courses at AICTE/UGC/MCI/BCI/AYUSH-recognised institutions across India.

Engineering: B.Tech, Diploma, MCA, M.Tech. Medical: MBBS, BDS, BAMS, BHMS, B.Sc Nursing, B.Pharm.

Management: MBA, PGDM. Polytechnic and ITI: BSBTE-affiliated courses.

Traditional degrees: BA, B.Sc, B.Com.

Check latest approved list at 7nishchay-yuvaupmission.bihar.gov.in under 'Approved Courses' before applying.

🔧Common issues and how to solve them

Issue: Application stuck at DRCC for weeks. Solution: Visit the DRCC in person and ask the officer for status.

Common bottlenecks: missing document (upload whatever's missing immediately), verification delay (the DRCC may be handling hundreds of applications - follow up weekly), or institution not on the approved list (check if your institution is recognized by UGC/AICTE before applying).

Issue: Loan disbursed but college demanding fees immediately. Solution: Show the college your BSCC approval letter and loan sanction order.

Most institutions familiar with BSCC accept the sanction letter as fee payment guarantee and allow you to attend classes while the disbursement is processed. If the college insists on immediate payment, contact the DRCC to expedite.

Issue: Want to change course or institution after loan approval. Solution: Visit the DRCC with the new admission letter and request a loan modification.

The DRCC can update the institution/course details. If the new course has higher fees, the adjustment is within the Rs 4 lakh limit.

If lower, the excess amount is cancelled.

Issue: Not a Bihar domicile but studied in Bihar. Solution: Unfortunately, BSCC requires Bihar domicile - studying in Bihar alone doesn't qualify.

If you're from another state, apply through Vidyalakshmi (bank education loan portal) or check if your home state has a similar student credit card scheme (West Bengal has a similar program, Odisha has one for ST students).

Women paid only 1% interest, and new loans are now 0%

For loans before September 2025, female Bihar students paid only 1% simple interest on the Rs 4 lakh loan. Total interest on Rs 4 lakh over 5 years at 1% was Rs 20,000.

New loans sanctioned from September 2025 carry 0% interest.

That's Rs 333/month in interest - essentially free financing for a 4-year degree. If you're a girl from Bihar who passed 12th and didn't go to college because of fees - this scheme removes your excuse.

Apply at 7nishchay-yuvaupmission.bihar.gov.in.

Apply BEFORE admission - don't wait until college starts

Apply for BSCC as soon as you get your 12th results - don't wait until you've taken admission. The loan processing takes 15-30 days after DRCC visit.

If you apply after college starts, you'll face fee payment deadlines before the loan is disbursed. Start the application process immediately after 12th results, even before admission confirmation.

BSCC Application Process

1

Register Online

Fill 7nishchay portal form

2

DRCC Verification

Visit DRCC with originals

3

Bank Sanction

BSEFC partner bank approves

4

Loan Disbursed

To college + student card

Bihar's Gross Enrollment Ratio in higher education was 15% - half the national average. Lakhs of 12th-pass students stopped studying because they couldn't afford Rs 20,000-50,000/year college fees. BSCC at 4% interest with no collateral has already helped 30+ lakh students. A girl from a village in Madhubani studying engineering in Patna on a Rs 4 lakh loan at 1% interest - that's what economic mobility looks like.

📈Success stories and scheme impact

Since launch in 2016, BSCC has processed over 30 lakh applications and disbursed loans to 20+ lakh students. The scheme has measurably increased Bihar's higher education enrollment - GER rose from 13% in 2016 to approximately 18% by 2025.

First-generation college students from rural Bihar - daughters of farmers, sons of daily wage workers - now study engineering, medical, and management courses that were financially impossible a decade ago.

The scheme has particularly benefited female students. With 1% interest (effectively free), the number of Bihar girls enrolling in higher education has increased by 40% since 2016.

In districts like Sitamarhi, Madhubani, and Araria (among Bihar's least developed), female enrollment has doubled. BSCC didn't just fund education - it changed the social equation around girls' education in rural Bihar.

Criticism and challenges: The Rs 4 lakh limit hasn't been revised since 2016 despite tuition inflation. Private engineering colleges that charged Rs 50,000/year in 2016 now charge Rs 80,000-1,00,000/year - stretching the Rs 4 lakh over 4 years.

Demand for increasing the limit to Rs 6-8 lakh has been growing. Also, processing delays at DRCCs (especially in peak admission season - July-September) cause students to miss fee payment deadlines.

🌐Other states with similar student credit card schemes

West Bengal Student Credit Card: Launched in 2021 with Rs 10 lakh loan at 4% interest. More generous than Bihar's Rs 4 lakh.

Covers courses in India and abroad. Apply at wbscc.wb.gov.in.

For West Bengal domicile students, this is among the best state-level education financing options.

Odisha Student Credit Card: Targets ST (Scheduled Tribe) students specifically. Provides Rs 10 lakh for higher education within India.

Interest is subsidized by the state government. Apply through the ST & SC Development Department portal.

Central schemes: Jan Samarth portal (jansamarth.in) connects students to education loans from multiple banks. Central Sector Interest Subsidy (CSIS) provides full interest subsidy during the moratorium period for students from families earning below Rs 4.5 lakh/year studying at IITs, NITs, and approved institutions.

PM Vidyalakshmi portal (vidyalakshmi.co.in) routes one application to multiple banks for education loans up to Rs 20 lakh.

If your state doesn't have a student credit card scheme, use Vidyalakshmi + Jan Samarth for bank education loans. Central government interest subsidy (CSIS) at zero cost covers the interest during study period for economically weaker families.

Check your state government's education department website - new student financing schemes are being launched frequently.

Official Sources & References

Source: Department of Education, Bihar Government. All information on this page has been verified against official government notifications and regulatory circulars.

For the latest updates, always check the official portal.

BSCC Timeline - Application to Disbursement

DAY 1

Online Registration

Fill 7nishchay portal

DAY 2-3

Document Upload

Marksheet, admission letter, Aadhaar

DAY 7-10

DRCC Appointment

Visit with originals + biometric

DAY 15-21

Bank Sanction

BSEFC sanctions loan

DAY 25-30

Loan Disbursed

Tuition to college

📝How to Apply

1

Register at 7nishchay-yuvaupmission.bihar.gov.in

Create account with mobile number → OTP verification → set password. First-time user setup.

2

Fill BSCC application form online

Personal details, 12th board and marks, family details and income, course and college details, bank account (salary account if possible), loan amount required (≤ ₹4L), nominee.

3

Upload documents online (JPEG, max 200KB each)

12th mark sheet, Aadhaar card, family income certificate (from Gram Pradhan/Tehsildar), domicile certificate (from district DM office), college admission letter, bank passbook (first page showing IFSC), passport photos (2, 4x6 cm).

4

Visit your district's DRCC with original documents

Usually within 60 days of online submission. Bring: all original documents, 2 photocopies, application ID. DRCC does biometric, verifies authenticity, counsels on repayment obligations. Takes 1-2 hours.

5

DRCC submits your verified application to state office

State level processes and sanctions loan (30-60 days from DRCC visit). You'll get notification via SMS/email when loan is sanctioned.

6

Loan amount disbursed in installments

Amount is sent directly to college (fee payment) and to your bank account (hostel, books, other expenses). Disbursement happens in 2-4 installments as per course structure (semester-wise or year-wise).

⚠️DRCC VISIT IS MANDATORY - Online application alone is NOT sufficient. You MUST visit your district's DRCC in person with original documents. Many students complete online application and expect automatic approval - this is wrong. Without DRCC verification, your loan will NOT be disbursed. Visit DRCC within 60 days of online submission. Details at 7nishchay-yuvaupmission.bihar.gov.in

📅Important Dates & Schedule

Online ApplicationOpen throughout the year at 7nishchay portal

DRCC Visit DeadlineWithin 60 days of online submission - delay means rejection

Loan Sanction30-60 days after DRCC approval

Disbursement2-4 weeks after sanction, in installments

Repayment Start1 year after course completion

Share this infographic

📌 You might also need

If the Scholarship Falls Short

Scheme amounts rarely cover the full cost of study. These cover the gap.

More Bihar Schemes

Schemes for Bihar residents you may also qualify for.

👷Bihar Labour Card: Apply, Status, Renewal, BOCW BenefitsBihar Labour Card (BOCW) gives registered construction workers pension,...🏪Bihar Laghu Udyami Yojana: Rs 2 Lakh Grant, Apply OnlineBihar Laghu Udyami Yojana gives poor families a Rs 2 lakh business grant...💍Kanya Vivah Yojana 2026: Marriage Aid for Poor Families₹5,000 to ₹51,000 marriage assistance for daughters from low-income...👩🎓Mukhyamantri Kanya Utthan Yojana: Last Date, Rs 50,000Mukhyamantri Kanya Utthan Yojana gives Bihar girl graduates Rs 50,000 and...

🛠️Payment failed or stuck? It is usually a name mismatchIf your Aadhaar and bank names differ even slightly, DBT credits bounce. Here is the exact fix, step by step

❓Frequently Asked Questions

7 Nishchay Portal

www.7nishchay-yuvaupmission.bihar.gov.in

🔗Related Schemes

Skill Development

PMKVY - Skill India

Girl ChildKanya Sumangala Yojana (UP)

Girl Child SavingsSukanya Samriddhi Yojana

BankingPM Jan Dhan Yojana

📋 Official Sources & Verification

Information verified against official government portals and gazette notifications. Read our editorial process.

Researched & verified from official sources

Last reviewed

June 2026

June 2026